Health Insurance Explained: How It Works and Why You Need It

Health Insurance Explained: How It Works and Why You Need It

Health insurance is one of the most important financial tools you can have in today’s world. Rising medical costs, unexpected emergencies, and long-term healthcare needs make health insurance essential for individuals and families across all countries, especially in Tier-1 regions such as the United States, Canada, the United Kingdom, Australia, and Europe.

In this comprehensive guide, we will explain how health insurance works, what it covers, how much it costs, and why having the right health insurance plan can protect both your health and your finances. This article is designed to help beginners and experienced readers alike make informed decisions.

What Is Health Insurance?

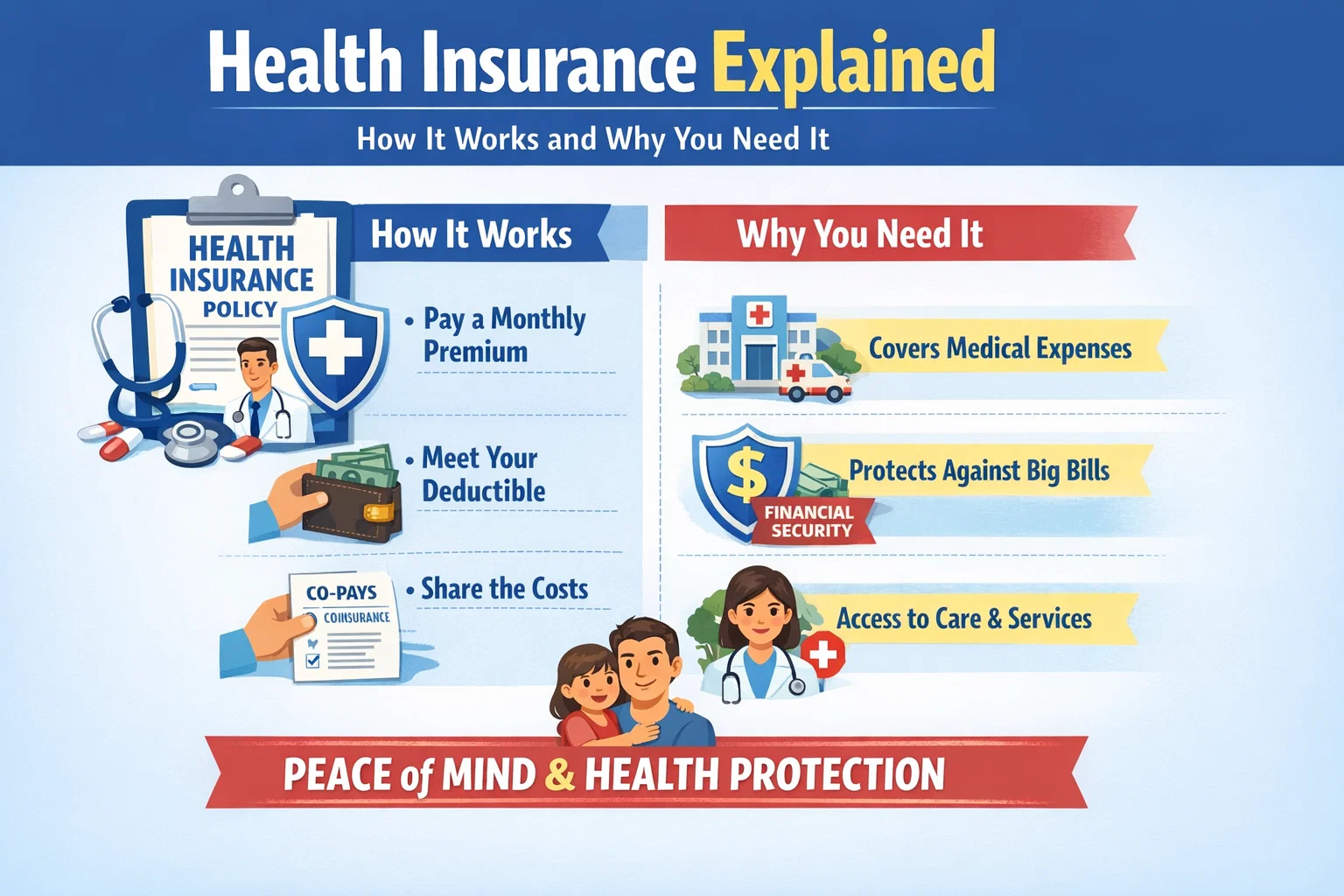

Health insurance is a contract between you and an insurance provider where the insurer agrees to cover a portion of your medical expenses in exchange for a regular premium payment. These expenses can include doctor visits, hospital stays, prescription medications, preventive care, and sometimes specialized treatments.

Instead of paying the full cost of medical care out of pocket, health insurance helps reduce financial risk by sharing costs between you and the insurer. This cost-sharing structure makes healthcare more affordable and accessible.

How Does Health Insurance Work?

Understanding how health insurance works is crucial before choosing a plan. Most health insurance policies follow a similar structure, regardless of country or provider.

Key Components of Health Insurance

- Premium: The amount you pay regularly (monthly or yearly) to keep your policy active.

- Deductible: The amount you must pay out of pocket before insurance coverage begins.

- Copayment (Copay): A fixed fee you pay for certain services, such as doctor visits.

- Coinsurance: A percentage of costs you share with the insurer after meeting your deductible.

- Out-of-Pocket Maximum: The maximum amount you pay in a year before the insurer covers 100% of eligible costs.

Once you understand these elements, it becomes easier to compare health insurance plans and determine which one aligns with your financial and medical needs.

What Does Health Insurance Cover?

Coverage varies depending on the policy, but most comprehensive health insurance plans include essential healthcare services that are highly valued by advertisers and insurers worldwide.

| Coverage Type | Description |

|---|---|

| Doctor Visits | Routine checkups, specialist consultations, and follow-up visits |

| Hospitalization | Inpatient care, surgeries, and overnight stays |

| Prescription Drugs | Coverage for approved medications |

| Preventive Care | Vaccinations, screenings, and wellness checkups |

| Emergency Services | Emergency room visits and urgent medical treatment |

Why Health Insurance Is Essential

Many people underestimate the importance of health insurance until they face a medical emergency. Even a short hospital stay can result in extremely high medical bills, especially in Tier-1 countries.

Health insurance provides financial security, peace of mind, and access to quality healthcare when you need it most. It also encourages preventive care, which can reduce long-term health risks and expenses.

Types of Health Insurance Plans

There are several types of health insurance plans available globally. Understanding these options helps you choose the right coverage.

- Individual Health Insurance: Designed for single policyholders

- Family Health Insurance: Covers multiple family members under one plan

- Employer-Sponsored Insurance: Provided through employers

- Private Health Insurance: Purchased directly from insurers

- Government-Supported Plans: Public healthcare or subsidized coverage

How Much Does Health Insurance Cost?

Health insurance costs depend on multiple factors, including age, location, health condition, coverage level, and provider network. Premiums in Tier-1 countries tend to be higher, but they also offer broader coverage and better healthcare access.

While lower-cost plans may seem attractive, they often come with higher deductibles and limited coverage. Balancing premium cost with coverage benefits is essential for long-term value.

How to Choose the Right Health Insurance Plan

Choosing the right plan requires evaluating both medical needs and financial capacity. Ask yourself:

- How often do I visit doctors?

- Do I need coverage for prescriptions?

- What is my budget for premiums and out-of-pocket costs?

- Do I prefer flexibility or lower costs?

Comparing multiple insurance providers and plans ensures you receive the best value for your money. This comparison process is also where high-CPC insurance keywords naturally apply.

Common Health Insurance Mistakes to Avoid

Avoiding common mistakes can save you money and prevent coverage gaps.

- Choosing the cheapest plan without reviewing coverage

- Ignoring deductibles and out-of-pocket limits

- Not checking network restrictions

- Failing to review policy updates annually

Health Insurance and Financial Security

Health insurance is not just about medical care—it is a critical part of financial planning. Unexpected medical expenses are one of the leading causes of financial stress worldwide.

By investing in a reliable health insurance plan, you protect your savings, income, and long-term financial goals while ensuring access to quality healthcare.

Final Thoughts

Health insurance is an essential safeguard in today’s uncertain world. Understanding how it works, what it covers, and how to choose the right plan empowers you to make confident decisions.

Whether you are an individual, a family, or a business professional, having the right health insurance coverage ensures peace of mind, financial protection, and access to the care you deserve.

Comments (3)